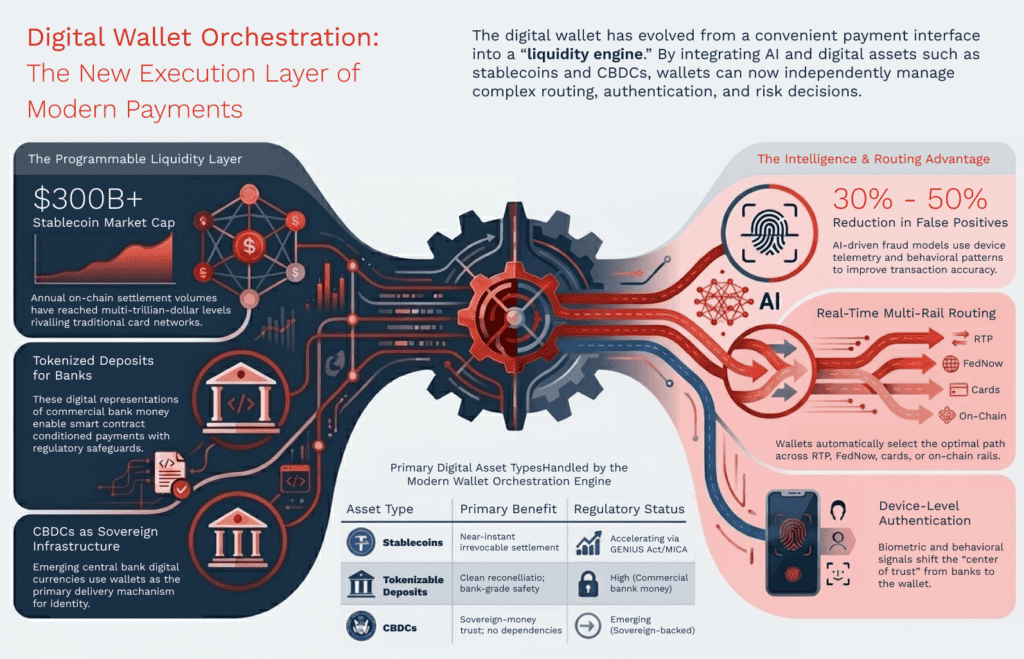

The digital wallet has quietly crossed a threshold. It is no longer a convenient interface layered over existing financial infrastructure — it has become the infrastructure. As stablecoins, tokenized deposits, and emerging central bank digital currencies enter mainstream financial flows, the wallet shifts from a payment front-end into something closer to a multi-asset liquidity engine: the point where money is held, routed, and increasingly, governed.

That shift has strategic consequences that most financial institutions have not yet fully priced in.

The most immediate signal is the stablecoin market. With market capitalization exceeding $300 billion (CoinMarketCap) and on-chain settlement volumes reaching multi-trillion-dollar levels annually, stablecoins have moved well past their speculative origins. They now function as a parallel settlement layer — used for platform payouts, cross-border remittances, and treasury operations — competing directly with card networks and correspondent banking rails on speed, cost, and programmability. The appeal is straightforward: price stability, near-instant irrevocable settlement, and the ability to embed payment logic directly into the instrument itself.

Regulatory clarity is accelerating institutional adoption. In the U.S., ongoing regulatory proposals in the U.S. are increasingly focused on reserve requirements, licensing, and AML/KYC frameworks for stablecoin issuers, licensing requirements, and AML/KYC frameworks designed to bring stablecoin issuers within the perimeter of regulated financial institutions. The EU’s MiCA framework and emerging APAC standards point in the same direction. The effect is predictable: as stablecoins become more governable, they become more viable as enterprise instruments — not just retail experiments.

Tokenized deposits take the logic one step further. Unlike stablecoins, whose backing sits outside the banking system, tokenized deposits are digital representations of commercial bank money. They bring bank-balance-sheet treatment and regulatory safeguards to programmable settlement — enabling near-instant multi-currency flows, smart-contract-conditioned payments, and cleaner reconciliation, without introducing the balance-sheet fragmentation that makes some institutions wary of stablecoins.¹ᐟ³ Early pilots suggest these instruments are emerging as the favored model for banks that want to modernize without losing their existing supervisory footing.

CBDCs remain the longest arc, but the direction is consistent. Central banks across Europe, Asia, and emerging markets are testing designs that combine sovereign-money trust with programmability and instant settlement. Their potential role in reducing correspondent banking dependencies — particularly for cross-border flows — is meaningful. What’s notable is that in almost every CBDC architecture under consideration, the wallet is the delivery mechanism: the layer responsible for identity management, consent, device-level security, and multiparty authorization.

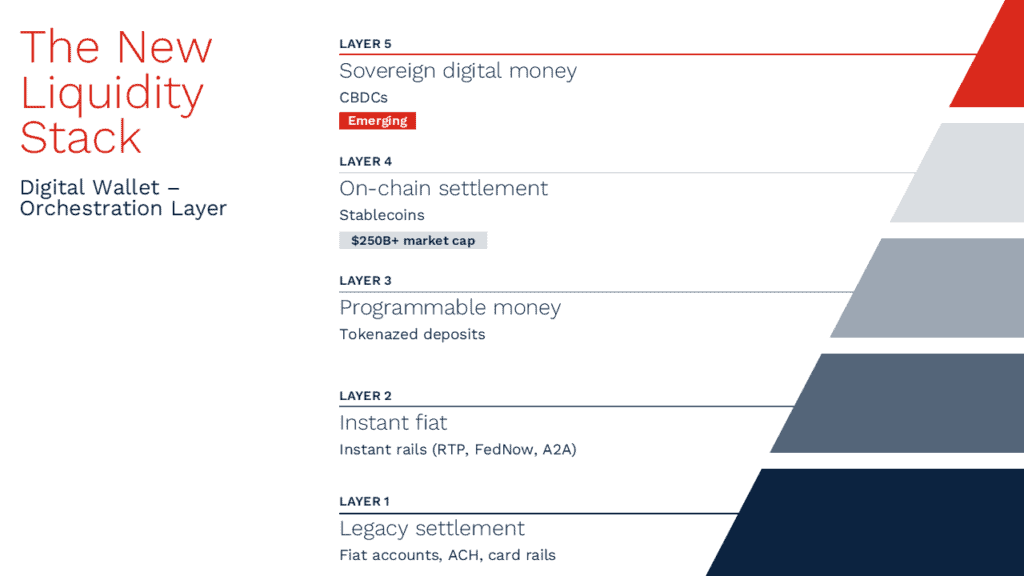

What ties these instruments together isn’t their technology. It’s their function. Stablecoins, tokenized deposits, and CBDCs all collapse settlement windows, reduce operational drag, and create new options for where and how liquidity moves. When integrated into wallets, they enable something that wasn’t possible before: real-time routing decisions that weigh bank rails, instant A2A networks, on-chain settlement, and tokenized deposits against each other — optimizing on cost, speed, corridor performance, and risk conditions simultaneously.

The wallet is no longer holding cards and fiat balances. It’s holding regulated token pools, stablecoin balances, tokenized deposits, CBDC sub-wallets — each on a distinct ledger, each with different operating rules. Orchestrating them coherently isn’t a UX problem. It’s an infrastructure problem, and the institutions that recognize that earliest will have a structural head start.

As digital wallet orchestration becomes a central capability in modern payments, institutions must rethink how execution, intelligence, and control are distributed across the stack.

Rail access used to be a competitive advantage. It isn’t anymore.

U.S. institutions now operate across RTP and FedNow instant rails alongside ACH, cards, and wallet-native flows — with RTP participation reaching over 70% of U.S. demand deposit accounts (The Clearing House), and FedNow continuing to expand its network of participating financial institutions following its 2023 launch (Federal Reserve). The infrastructure is broadly accessible. What separates execution quality isn’t which rails an institution can reach: it’s the intelligence applied at the moment a transaction is initiated.

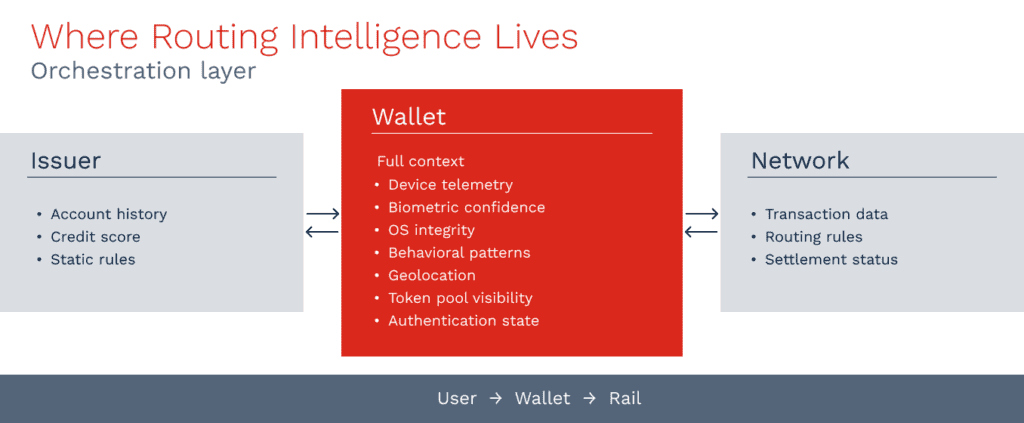

That intelligence now lives in the wallet.

Wallets occupy a position in the payments stack that neither issuers nor processors can fully replicate. They hold device-level context: biometric confidence scores, OS integrity signals, behavioral telemetry, geolocation consistency, persistent interaction history. When a transaction initiates, a well-architected wallet isn’t simply passing credentials downstream — it’s running a real-time evaluation of which rail offers the optimal combination of approval likelihood, fraud risk, corridor performance, and cost. Machine learning models make those calls in milliseconds, drawing on signals that a card issuer, sitting further back in the stack, cannot access at the same granularity.

The practical result is already visible. In ecosystems where wallet-layer authentication is mature, wallets consistently maintain higher approval rates than the underlying card issuers — because the context they bring to each transaction is richer and the authentication certainty is higher. That’s not a temporary dynamic. As multi-rail complexity grows, the wallet’s informational advantage compounds.

Liquidity decisioning is the next frontier. As digital assets integrate, routing choices expand beyond cards and instant rails to include stablecoin pools, tokenized deposits, and eventually CBDC channels. Stablecoins already settle more than $20 billion in daily on-chain transactions — a volume that makes them a credible execution option, not a theoretical one. Wallets that hold visibility into user balances, asset types, token pools, and authentication state are better positioned than any issuer to determine which ledger should execute a transaction and under what conditions: whether the FX spread favors on-chain settlement, whether a tokenized deposit path reduces counterparty latency, whether corridor performance on a given instant rail has degraded in the last 90 seconds.

The structural parallel worth noting is the mobile operating system. A decade ago, OS platforms became the policy-enforcing layer for app ecosystems — governing identity, permissions, and access in ways that neither developers nor telecoms could override. Wallets are performing the same function in payments: setting authentication standards, interpreting identity signals, initiating routing decisions, and shaping transaction quality before a bank or network ever sees the instruction. The more rails that exist, the more valuable that orchestration position becomes.

For financial institutions, the honest question isn’t whether to participate in multi-rail environments — that decision has already been made by the market. The question is where in the stack they intend to compete. Rail access is commoditizing. Execution quality: early fraud detection, optimal path selection, liquidity-aware routing, real-time token eligibility checks — is not. Institutions that integrate with or build wallet-native orchestration capabilities will be able to deliver consistent, policy-bound execution across every rail in the stack. Those that don’t will find themselves increasingly dependent on interface layers they don’t control, executing instructions they didn’t shape.

If the wallet is the orchestration layer, AI is what makes orchestration possible at scale.

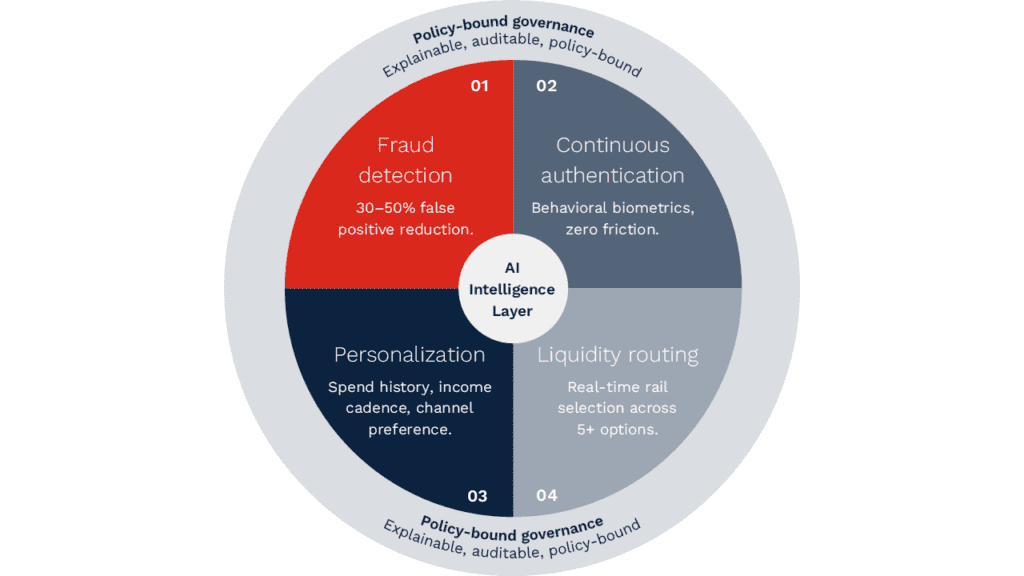

The case starts with fraud. Traditional rule sets were designed for a world where settlement had friction — where a disputed charge could be reversed, a suspicious pattern could be flagged for review, and a false positive meant a delayed transaction rather than a permanent loss. Instant settlement changes the physics of the problem. When finality is immediate and reversibility is constrained, the cost of a wrong call — in either direction — is categorically higher. AI-driven fraud models address this by ingesting behavioral patterns, device telemetry, biometric confidence scores, geolocation drift, and enriched ISO 20022 fields to generate anomaly scores in real time. Early adopter environments are reporting measurable improvements in fraud detection accuracy and real-time decisioning. That’s not an incremental improvement; it’s a structural shift in how risk gets managed at the transaction level.

Authentication is where the wallet’s hardware advantage becomes most visible. Wallets already operate at the device layer — secure enclaves, OS-level attestation, biometric hardware. AI extends this into continuous authentication: typing cadence, accelerometer patterns, touch dynamics, evaluated passively throughout a session to maintain identity confidence without introducing friction. The practical effect is that step-up challenges become rare, targeted events rather than default friction points. More consequentially, the center of trust shifts. Increasingly, it is the wallet’s identity engine — not the issuing bank — that governs the confidence level attached to each transaction.

Personalization follows the same logic. Wallets accumulate granular data that no issuer or processor can match: merchant-level spend classification, income cadence, channel preferences, behavioral patterns across thousands of interactions. AI converts these signals into recommendations that feel contextual rather than algorithmic — micro-savings nudges, credit offers timed to a user’s actual financial cycle, merchant-specific promotions delivered before checkout rather than after. The gap between what a wallet can offer here and what a bank app can offer is already wide. It will widen further as conversational interfaces mature. Natural-language queries, payment initiation by voice, proactive budgeting alerts — these are already in deployment at scale in several markets. The wallet stops being a tool the user navigates and becomes something closer to a financial counsel that acts.

None of this works without governance. As regulators expand oversight of automated decision systems, AI models embedded in wallets will need to be explainable, auditable, and tied to defined decision frameworks. Drift detection, bias monitoring, and explainability layers aren’t optional components — they’re the condition under which regulators will permit these systems to operate at the level of autonomy they’re capable of. Institutions that build this infrastructure now will find it a competitive asset; those that treat it as a compliance burden will find it an operational constraint imposed from outside.

The wallet was, not long ago, a convenient shortcut to a card network. It is now the point where authentication, routing, liquidity, personalization, and compliance converge — governed by AI, operating across multiple ledgers, in real time. Financial institutions that recognize this as infrastructure rather than interface will be positioned to lead the next decade of payments. Those that don’t will find themselves executing on terms set by someone else’s platform.

- CoinMarketCap — Stablecoin Market Capitalization Data (2024–2025).

- Visa — The Future of Money Movement: Stablecoins and Blockchain (2024).

- The Clearing House — RTP Network Overview and Statistics (2024–2025).

- Federal Reserve — FedNow Service: Participating Financial Institutions (2024–2025).

- European Commission — Markets in Crypto-Assets (MiCA) Regulation (2024–2025).

- U.S. Payments Forum — Mobile & Digital Wallets: Updated U.S. Landscape and Strategic Guidance (2025).

- The Payments Association — The Evolution of Digital Payments and Consumer Trends (2024–2025).

- Mastercard — Insights on Digital Wallets and Payment Innovation (2023–2024).