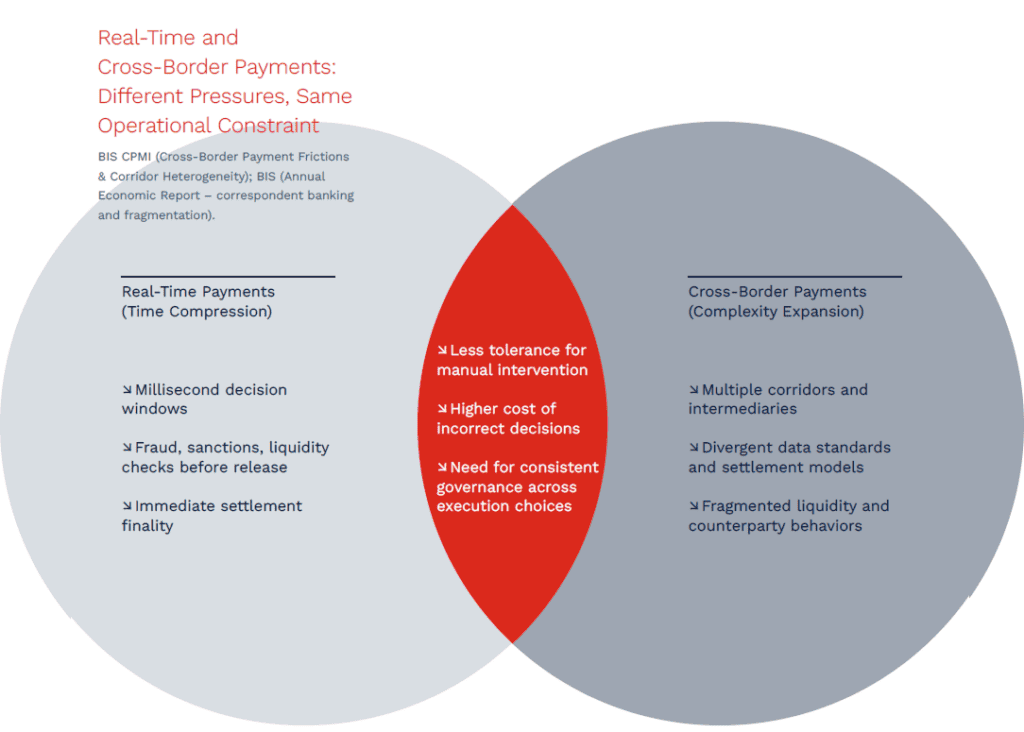

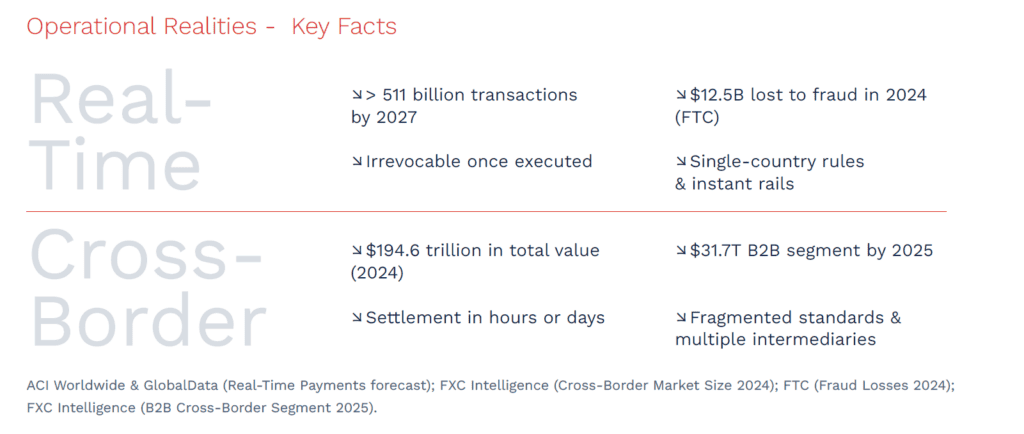

Domestic real-time payment rails such as RTP® and FedNow® have pushed the U.S. from episodic, batch-based processing into continuous execution. Fraud screening, sanctions checks, liquidity verification, and routing decisions must occur before a payment is released—and once released, reversibility is extremely limited. This compression of the control window exposes weaknesses that batch-based models once obscured. Exceptions that could previously be resolved after the fact now surface as outright failures if not prevented at initiation.

Cross-border payments do not compress time in the same way, but they introduce a different form of pressure: heterogeneity. Payments traverse corridors with divergent data standards, settlement models, liquidity regimes, and counterparty behaviors. Rather than converging, the cross-border landscape continues to fragment across correspondent banking, regional instant-payment systems, digital wallets, and token-based settlement paths.

The operational complexities introduced by this landscape are magnified by its sheer scale. The total value of cross-border payments was estimated at $194.6 trillion in 2024, with the B2B segment alone expected to account for $31.7 trillion in 2025. Despite this immense scale, the environment remains fragmented across standards and settlement layers. To address this, the Financial Stability Board (FSB) has established an ambitious goal: by 2027, 75% of all cross-border payments should settle within one hour.

At the same time, domestic instant rails introduce risks that demand smarter safeguards. In the U.S. alone, fraud-related losses exceeded $12.5 billion in 2024, according to the FTC. The speed and irrevocability of real-time payments amplify the cost of poor controls. The convergence of these pressures creates an imperative: shift governance upstream, enable pre-release intelligence, and ensure coherence across execution paths.

Despite these differences, the operational reality is increasingly similar. Both environments present more execution choices, less room for manual intervention, and higher consequences when decisions are wrong. In both cases, competitiveness depends on making better decisions earlier—and governing them consistently across complexity.

Conclusion

Key common prerequisites: early decision intelligence, AI-enabled governance, and coherence across execution paths.

Banks today operate across more rails than ever: ACH, RTP®, FedNow®, card networks, wallets, and multiple cross-border pathways. Access to rails has become commoditized. What differentiates institutions is no longer connectivity, but execution quality across choice.

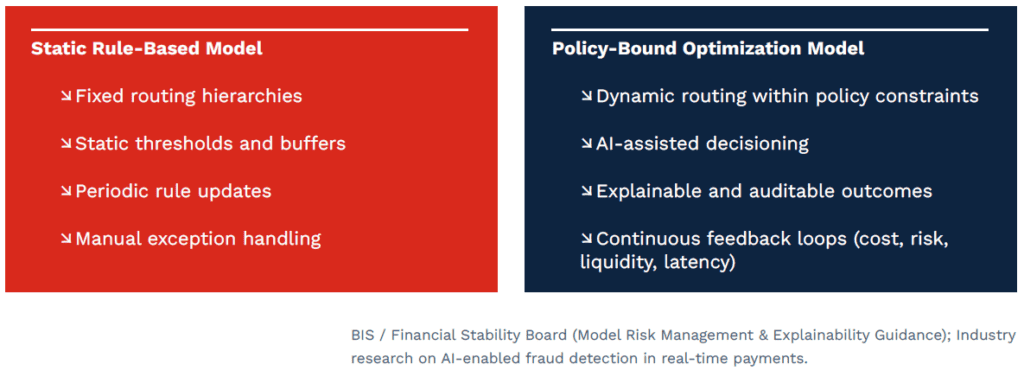

Static routing rules, once a source of stability, are increasingly brittle. Rail availability, fraud patterns, liquidity positions, FX spreads, and counterparty uptime now fluctuate intraday. Institutions that rely on conservative defaults—higher prefunding buffers, rigid routing hierarchies, and expanded manual review—often reduce risk locally while quietly eroding cost efficiency and customer experience systemically.

RTP® now supports more than 1,000 banks, covering over 70 percent of U.S. Demand Deposit Accounts, while FedNow® surpassed 1,500 institutions across all 50 states by late 2025. These two independent, non-interoperable instant rails have accelerated dual-rail adoption, but dual-rail connectivity alone creates its own complexity. Routing decisions across ACH, RTP®, FedNow®, card push, wallets, and tokenized paths are too complex to maintain via manually curated rules.

Leading processors treat rails as modular components, dynamically selecting paths based on cost, risk, liquidity, uptime, and user experience. Without intelligent, policy-bound orchestration, additional rails simply increase operational load.

This shift in value creation is measurable. A 2024 Statista survey found that 39% of merchants have stopped working with a payment provider due to high rates of falsely declined transactions. In an environment where execution errors directly impact revenue and trust, institutions that rely on rigid, rule-based systems risk losing their most valuable clients—not due to a lack of rails, but a lack of accuracy.

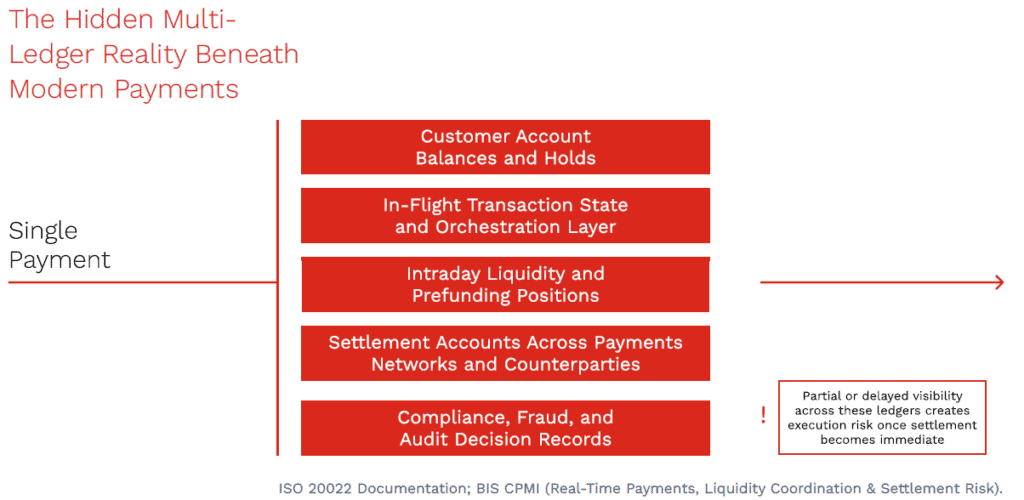

Misalignments were tolerable because settlement was slow and reversible. In real-time and cross-border environments, this fragmentation becomes a structural weakness. Decisions made on partial or lagging views of ledger state produce unpredictable outcomes. Many payment failures are not rail failures—they are ledger misalignments revealed too late.

ISO 20022 improves the situation by enabling richer, structured payment data and better automation. However, messaging standards alone do not resolve multi-ledger fragmentation. Institutions still rely on static thresholds, periodic liquidity buffers, and siloed rule engines. As complexity increases, the instinctive response is to tighten controls at the edges—larger buffers, more manual checks, and more rigid routing—reducing risk while increasing cost and opacity.

The solution is not ledger consolidation, but orchestration: interpreting multiple ledger states in real time and applying them consistently within execution decisions. An orchestrator operates as a real-time coordination layer above existing ledgers and control systems, continuously synthesizing liquidity, risk, compliance, and accounting states into a unified operational view. Rather than replacing underlying systems, it ensures that routing, sequencing, funding, and limit enforcement decisions are made against a synchronized, current multi-ledger position. Coherence, therefore, is achieved not by merging ledgers, but by coordinating them at the point of execution.

Despite their critical role, these ledgers have historically existed in silos—often governed by separate systems, owners, and departments. This fragmentation is not merely conceptual. According to the Bank for International Settlements (BIS), “compartmentalized organizational structures may hinder effective linking of data, as the information tends to be guarded by its owners in ‘data silos’.” The BIS also notes that fragmented data environments often result in “inconsistent formats and sources… leading to inefficiencies and redundant data storage.” In a real-time payments ecosystem, this disconnection across risk, compliance, and liquidity layers can create operational blind spots at precisely the moments when coherence is most critical.

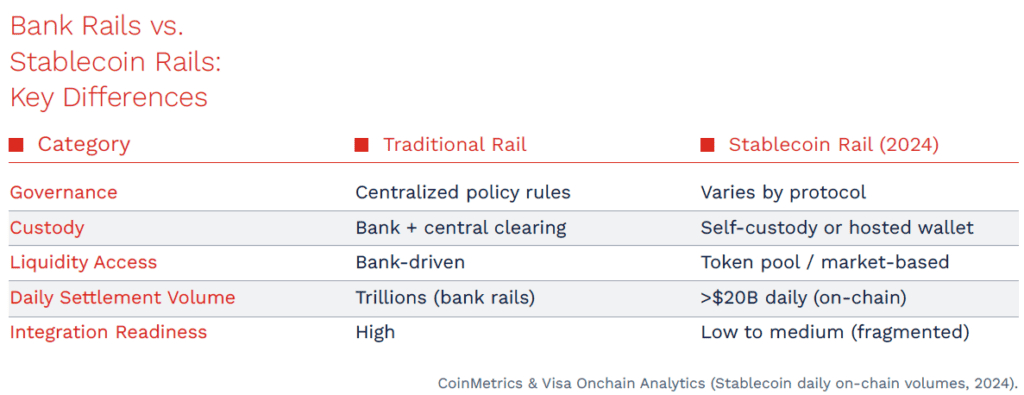

Stablecoins are beginning to appear in specific commercial payment flows, including platform payouts, select cross-border corridors, and corporate treasury transfers. They do not replace existing rails; they add another execution option. Operationally, this introduces yet another ledger—with distinct liquidity dynamics, custody models, regulatory requirements, and FX implications.

Stablecoin adoption is growing rapidly, not only in retail crypto markets, but also in commercial and cross-border payment use cases. As of early 2024, the total market capitalization of stablecoins exceeded $124 billion, and daily on-chain transfer volume reached over $20 billion—figures that reflect increasing usage in enterprise treasury, B2B payments, and remittances. This growth highlights their relevance as an emerging rail—but also reinforces the need for integration with orchestration frameworks. Without governance and compatibility controls, stablecoins risk becoming yet another isolated layer—adding operational burden rather than solving it.

Without integration into the broader orchestration framework, stablecoin usage remains niche and operationally constrained. Once integrated, stablecoins become one more governed settlement option—evaluated alongside traditional rails based on eligibility, risk, liquidity, cost, and explainability.

Regulated stablecoins in APAC now settle significant trade-finance volumes, and early U.S. frameworks such as the GENIUS Act propose audited reserves and strong AML/KYC standards. The rise of stablecoin settlement in global commerce reinforces the need for multi-ledger orchestration and decision frameworks that evaluate stablecoins like any other rail—based on eligibility, risk, liquidity, and explainability.

“Without orchestration, stablecoins function as isolated rails — requiring the same risk, liquidity, and explainability standards as any other settlement layer.”

Legacy operating models rely on rules that were designed for batch environments: static limits, predetermined routing pathways, fixed risk categories, and limited context for exceptions. These rules cannot adapt to conditions that change intraday.

When routing, fraud, liquidity, and compliance decisions operate independently, outcomes may be locally correct but globally inefficient. Institutions are therefore moving toward rail-agnostic orchestration, where optimization operates within policy boundaries, rather than replacing policy altogether.

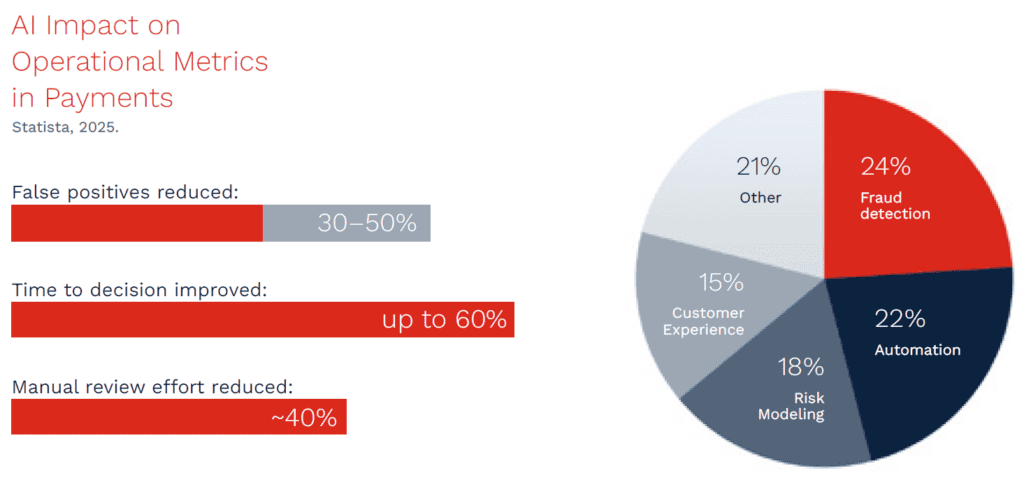

AI’s impact is not theoretical — it can be measured in tangible outcomes. Across the financial industry, AI-powered fraud detection systems have been shown to reduce false positives by 30% to 50%, improving both risk management and customer experience. A 2025 Statista survey found that 24% of banking organizations identify enhanced fraud detection and cyber-attack response as the primary benefit of AI adoption. Furthermore, the broader fintech AI market is projected to grow at a CAGR of 23.7% through 2030, driven largely by AI use cases in automation, liquidity forecasting, and risk orchestration. Taken together, these figures demonstrate that AI is more than a conceptual layer—it is a measurable driver of operational resilience and competitive advantage in modern payments.

AI is equally transformative in compliance. Batch-based screening is incompatible with RTP® and FedNow®. Machine-learning models perform entity resolution and contextual scoring in real time, reducing operational burden and improving accuracy. AI also extends into routing and rail selection, evaluating cost, liquidity impact, latency, and risk conditions to determine the optimal path. Treasury teams benefit as well: AI strengthens intraday liquidity forecasting by predicting flow patterns and recommending funding adjustments. These capabilities allow institutions to handle continuous settlement without resorting to overly conservative liquidity strategies.

Governance must anchor AI use. Decisions must follow policy boundaries, and AI outcomes must be explainable. Institutions must capture decision trails that link policy, data, model, and outcome so auditors, risk teams, and regulators can validate why a payment was executed a certain way. AI does not replace governance; it operationalizes governance at the speed and complexity required by modern payments.

Full-stack reinvention is not a call to replace core systems. It is a shift toward aligning how decisions are made and executed across channels, rails, and ledgers. Payments leaders are reorganizing around an orchestration “center of gravity,” where policy, risk, liquidity, and routing come together. This orchestration layer coordinates decisions while leaving underlying systems intact. It becomes the engine through which domestic real-time payments, cross-border pathways, card networks, wallets, and stablecoin settlement can be governed consistently.

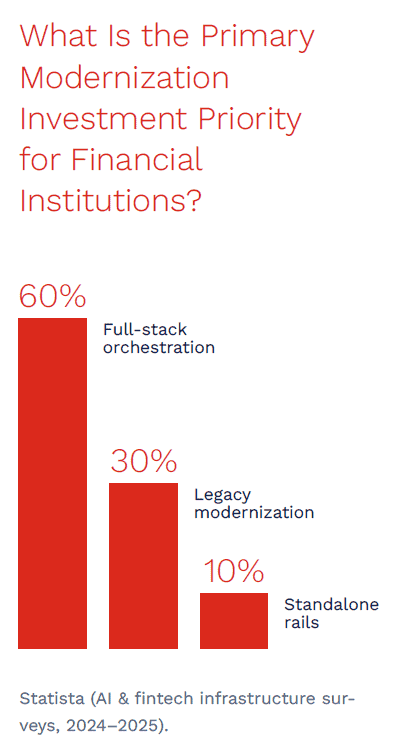

The trend toward full-stack orchestration is measurable. Recent industry surveys show that over 60% of global financial institutions prioritize investments in full-stack decisioning and orchestration platforms as key modernization objectives. These platforms are not just architectural evolutions — they deliver tangible operational benefits. Institutions that integrate full-stack models report up to 40% reductions in settlement and reconciliation cycle times, enabling faster liquidity availability and lower operational risk.

Ledger awareness is foundational. Instead of consolidating ledgers, institutions improve synchronization and visibility: real-time customer balances, execution states, treasury positions, and settlement states must be surfaced with minimal lag. Modern ISO 20022-based messaging and real-time treasury tooling are enabling better coordination without demanding monolithic architecture.

Institutions that embed governance directly into execution—bringing payments, treasury, risk, compliance, and technology into shared decision frameworks—gain resilience and transparency as complexity grows.

Speed is no longer a differentiator. RTP® and FedNow® have made it available to nearly all U.S. institutions. Cross-border modernization is expanding the set of choices. Differentiation between 2025 and 2030 will hinge on the ability to govern payments once execution becomes immediate and fragmented.

Leading institutions will treat domestic real-time payments, cross-border flows, and emerging settlement options as a single decision system—governed by common context, policy, and intelligence. Those that restore coherence—through multi-ledger orchestration and AI-driven optimization—will manage complexity deliberately rather than defensively.

The future belongs to financial institutions—banks, fintechs, and digital asset platforms alike—that can make sound decisions consistently and explain why those decisions were made. In an ecosystem defined by immediacy and fragmentation, competitive advantage comes not from faster rails, but from coherent execution at scale.

As the global digital payments market is projected to reach $26.89 trillion in transaction value by 2026, the competitive frontier clearly lies not in connectivity alone, but in mastering coherent execution across systems and rails.

Understand how real-time and cross-border payments are converging, the operational challenges this shift creates, and how multi-ledger orchestration and AI-driven optimization are redefining execution in modern payments.

Complete the form to download the full article.

By clicking “Submit,” you agree to receive communications from BIP US.