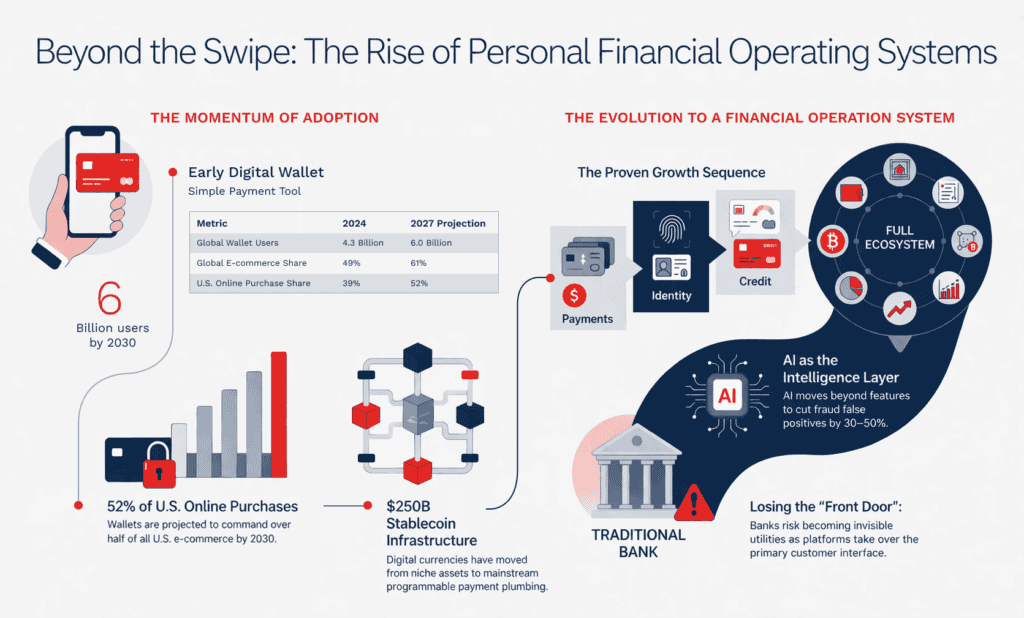

Digital wallets are rapidly evolving beyond payments, becoming a central element in how consumers manage their financial lives. As digital currencies and embedded finance expand, wallets are increasingly acting as the foundation of integrated financial ecosystems.

As illustrated above, the wallet is no longer a payment method. It’s the interface through which consumers increasingly manage their entire financial lives: payments, identity, credit, loyalty, and digital assets consolidated into a single environment they actually trust. That shift has been building for years. What’s changed is the pace.

Two dynamics are accelerating it simultaneously: mobile-first adoption that has made the device the default financial terminal, and the rise of super-app ecosystems where the wallet becomes the home screen for financial life. Underneath both, instant account-to-account networks have removed the last meaningful friction from fund movement. None of this is reversible. Together, these forces are compressing a decade of predicted change into a much shorter window.

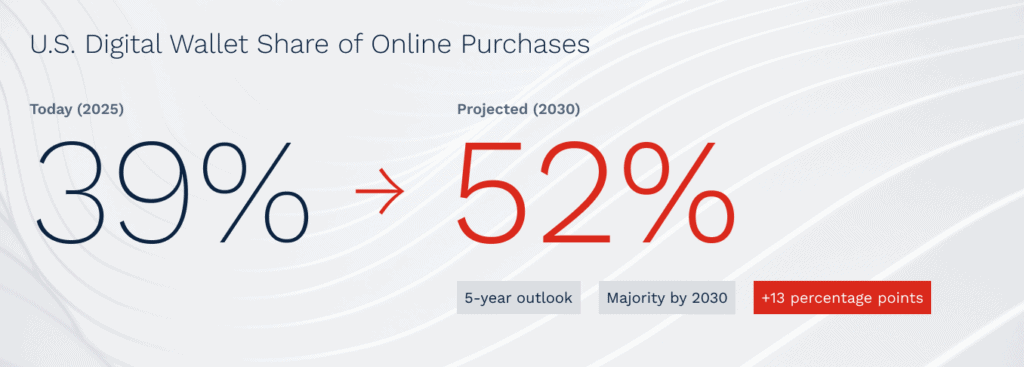

The economics are following the interface — and that’s the part institutions need to watch. In the U.S., wallets account for approximately 39% of online purchases today and are projected to reach 52% by 2030. Control of the wallet increasingly means control of the customer relationship, the transaction data stream, and the cross-sell economics that flow from both.

Digital currencies, particularly stablecoins, are no longer a parallel story. Stablecoin market capitalization has surpassed $250 billion, and on-chain settlement volumes now run at multi-trillion-dollar annual levels. Stablecoins and tokenized money have crossed from niche to infrastructure, bringing programmable liquidity into mainstream payment flows. As regulatory regimes clarify, the wallet becomes the execution layer for digital money spanning fiat accounts, token pools, and future CBDC interfaces. The plumbing is changing underneath the interface.

Speed, at this point, is table stakes. When execution is immediate across multiple rails, the competitive advantage shifts upstream: to decisioning. Who governs routing? Who manages identity, liquidity, and compliance before the transaction releases? That’s where AI earns its place, not as a product feature, but as the intelligence layer that makes the whole system coherent. Cutting fraud false positives by 30–50% matters, but the larger prize is a system that can make policy-bound decisions at speed and scale across every rail simultaneously. That’s a personal financial operating system. Not a faster app.

The question institutions should be asking isn’t whether wallets will evolve into PFOS: that’s already underway. The question is whether they’ll be inside that evolution or outside it. The real risk isn’t disruption. It’s irrelevance. The institutions that delay won’t lose to better banks. They’ll lose to platforms that never asked permission to become financial infrastructure in the first place.

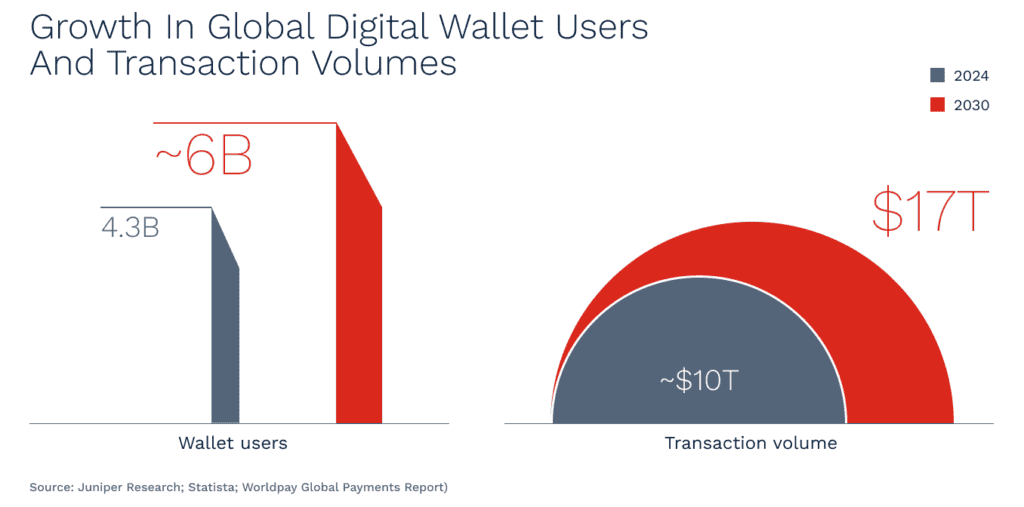

The numbers tell part of the story. Digital wallet users are projected to grow from 4.3 billion in 2024 to nearly 6 billion by 2030; transaction volumes over the same period climb from roughly $10 trillion to $17 trillion, according to Juniper Research and Statista. But the more important shift isn’t volume — it’s architecture. Wallets have moved from credential stores to the primary interface through which consumers manage payments, identity, loyalty, savings, and digital assets. The device is no longer a channel. It’s the operating base.

In leading digital wallet markets such as Asia-Pacific, it makes the end state legible. WeChat Pay, Alipay, GrabPay, and Paytm have crossed 90%+ penetration in major urban markets, for payments, identity, commerce, rewards, and lending within a single interface. The lesson isn’t that super-apps are culturally specific. It’s that once a wallet becomes the primary financial touchpoint, the interface displaces the account as the organizing principle. Consumers stop thinking about their bank. They think about their app.

This dynamic is also playing out in the U.S., with digital wallets evolving at a different pace, just more slowly. The 39% → 52% trajectory in online purchases is being driven by tokenized credentials and biometric authentication that simply outperform browser-based checkout in both security and speed. What Asia reached through super-app ecosystems, Western markets are arriving at through a different path and at a different pace — but arriving nonetheless.

Within the digital wallet ecosystem, the identity dimension is where the strategic stakes sharpen. Device-local biometrics, secure enclaves, attestation certificates, and tokenized credentials now allow wallets to authenticate with a precision that bank apps rarely match. Trust is migrating from the issuing institution to the interface layer. The wallet, not the bank, increasingly determines authentication quality, behavioral signal richness, and transaction release confidence. That’s not a UX detail.

It’s a reallocation of institutional authority.

As digital wallets become the primary interface, wallet providers now hold advantages that issuers spent decades building: deep device-level context, stronger authentication, and continuous visibility into spending behavior. They shape approval outcomes, influence routing, and govern cross-sell access. Banks aren’t losing customers yet. They’re losing the front door. And in financial services, whoever owns the front door owns the relationship.

Integrating into the wallet layer has crossed from strategic option to competitive necessity. Institutions that remain outside it face a specific and underappreciated risk: not just losing payment volume, but losing the behavioral data and engagement frequency that make every other product decision possible. The digital wallet is the new center of gravity. The only real question is whether institutions position themselves around it, or get pulled into its orbit on someone else’s terms.

In the evolution of digital wallets, PayPal didn’t set out to become a bank. Neither did Cash App. But both now offer deposits, investing, credit, and tax services alongside their original P2P payment functions. Cash App’s inflection point was the Cash Card: a debit card linked to the app balance that turned a P2P tool into a primary spending account. Once users started routing their paychecks through it, the expansion into investing and tax services became inevitable. That trajectory isn’t accidental. It’s the PFOS logic playing out in real time: once a wallet owns the payment moment, it owns the context for everything adjacent to it.

A Personal Financial Operating System isn’t a super-app rebrand. It’s a structural shift in how financial products are delivered: payments at the core, but triggering a continuous set of decisions: liquidity forecasting, automated savings, credit provisioning, micro-investing, budgeting, merchant-level personalization. These capabilities aren’t bolt-ons; they run on the same behavioral data, authentication signals, and interaction frequency that the payment function generates. The wallet earns the right to offer credit because it already knows the spending pattern. That’s not a feature. It’s a structural advantage that traditional product silos can’t replicate.

The global data reflects how far this has already progressed. Wallets accounted for 49% of global e-commerce payments in 2023 and are projected to reach 61% by 2027, per Worldpay’s Global Payments Report. Wallet users will approach 6 billion by 2030. These aren’t adoption curves — they’re consolidation curves. Financial activity is concentrating at the interface layer, and the interface layer is increasingly controlled by non-banks.

Asia established the blueprint. WeChat integrates payments, commerce, insurance, credit, and savings for more than 1.3 billion monthly active users; Alipay and GrabPay have achieved comparable depth across Southeast Asia. The lesson Western institutions keep drawing from Asia is about scale. The more relevant lesson is about sequence: payments came first, then identity, then credit, then everything else. The digital wallet didn’t start as a financial operating system. It became one because it had the data and the daily interaction frequency to justify each expansion.

![[Site US] Article Digital Wallets & Digital Currencies 3 [1]](https://www.bipconsulting.us/wp-content/uploads/2026/03/Site-US-Article-Digital-Wallets-Digital-Currencies-3-1.png)

![[Site US] Article Digital Wallets & Digital Currencies 3 [2]](https://www.bipconsulting.us/wp-content/uploads/2026/03/Site-US-Article-Digital-Wallets-Digital-Currencies-3-2.png)

![[Site US] Article Digital Wallets & Digital Currencies 3 [3]](https://www.bipconsulting.us/wp-content/uploads/2026/03/Site-US-Article-Digital-Wallets-Digital-Currencies-3-3.png)

![[Site US] Article Digital Wallets & Digital Currencies 3 [4]](https://www.bipconsulting.us/wp-content/uploads/2026/03/Site-US-Article-Digital-Wallets-Digital-Currencies-3-4.png)

That sequence is now repeating in Western markets — just through different entry points and at a pace shaped by regulatory environment and consumer trust levels. The direction is the same. And the economics are punishing for institutions that wait. A single wallet interface can cross-sell multiple financial products at negligible marginal cost, with acquisition economics that bank branch models cannot approach.

For financial institutions navigating digital wallet ecosystems, the strategic choice is real and uncomfortable. Integrating into wallet ecosystems preserves relevance in high-frequency flows but accelerates the erosion of direct customer relationships. Building PFOS-like capabilities internally means confronting orchestration complexity, data unification, identity governance, and multi-rail payment integration simultaneously — none of which are small lifts. There’s no clean path. But there is a clear cost to inaction: institutions that neither integrate nor build will find themselves holding the account while someone else holds the relationship.

The operating model shift, in the end, is simple to state and hard to execute: from managing products to managing context. The right decision, the right risk posture, the right offer — delivered at the moment of interaction, not surfaced later in a separate app that the customer opens twice a month.

- Worldpay. Global Payments Report 2024. Digital wallet adoption, mobile-first usage trends, and the rise of wallets as primary payment interfaces.

- Worldpay. Global Payments Report 2025. U.S. e-commerce payment mix, digital wallet share, and 2030 adoption forecasts.

- CoinMarketCap; Circle. Stablecoin market size and on-chain settlement trends, including total stablecoin market capitalization surpassing $250B and annual settlement volume benchmarks, 2024–2025.

- Global Treasurer. “How AI Is Reshaping Fraud Detection in Payments,” 2025; Resolve. “8 Statistics Pointing to Increased Fraud Detection via Machine Learning,” 2025.

- Juniper Research. Digital wallet global user projections toward ~6 billion by 2030, 2025.

- Statista. “Digital Payment Trends Worldwide,” 2026. Global digital payment transaction volume estimates.

- Corbado. “Digital Wallet Assurance: EU, US, and Australian Frameworks,” 2025; Entrust. “The Future of Payment Wallets and Identity Security,” 2025.

- U.S. Payments Forum. “Mobile & Digital Wallets: Updated U.S. Landscape & Strategic Guidance,” 2026.

- Mastercard. Digital Wallets 2022–2026, 2023.

- The Payments Association. “The Evolution of Digital Payments and Consumer Trends,” 2025.

- Entrust. “The Future of Payment Wallets and Identity Security,” 2025.